Why More People Are Moving Away from PayPal

-

Aaron Gray

- Blogs

-

July 16 , 2021

July 16 , 2021 -

6 min read

6 min read

When it launched, PayPal was one of the only ways to safely pay for online purchases. Now, there are more options than ever before

Money has taken many forms over the years. Initially, currency consisted of rare objects found in nature. This could be shells, stones, beads, copper, gold or even animals. From these forms, money eventually developed into coinage, favoured for its portability and durability. Importantly, currency of all forms became a form of political control over subordinate classes. (1)

Jump to the 21st century and money has once again changed face – this time going digital. In the digital payment industry, it’s PayPal which is the leader of the pack. PayPal maintains dominance in this space for a number of reasons, but the biggest is by virtue of being the first company to process digital payments.

Their maturity has helped PayPal to understand the payments industry better than most, but that doesn’t mean they’ve stayed ahead of the pack. Not by a long shot. People are moving away from PayPal, and in this article, we look at why exactly that is.

1. Fees

There are currently 392 million accounts (and counting) on PayPal and the company makes much of its revenue in dollars from the fees that customers pay when using its platform. Ordinarily, these fees are at a fixed rate of 2.9% and 30c per transaction, but competing platforms are challenging this hegemony with fees of roughly 2-2.5%.

PayPal’s market dominance has had an enabling effect on their fees so, unsurprisingly, we’re about to see some changes. Some of the new fees in their revised process include:

- For the following products, the fees will now be 3.49% + 0.491c: PayPal Checkout, PayPal Pay with Rewards, Pay in 4, Pay with Venmo, PayPal Credit, Pay in 4 and PayPal Credit and Checkout with Crypto.

- In-person payments will incur a new rate of 2.4% + 0.5c for payments over $10

- Online debit and credit card transactions will have a fee of 2.59 + $0.491

- Charity donations will have a new rate of 1.99% + 0.49c. (2)

In contrast, many of PayPal’s competitors are using its complex fee structure to position their services as more desirable. They do this by reducing fees or implementing a simpler, more transparent process.

2. Poor customer support

Many new financial products and digitally based businesses are turning huge profits in part because they lack physical branches for customers. PayPal are beneficiary of exactly this structure, but there is a downside for the consumer. Users seeking help, advice, or answers must navigate a convoluted phone and email process to get support.

As a third-party payments platform, PayPal encounters disputes between buyers and sellers, often siding with the buyer. However, their handling of mistakes, like sharing incorrect information between transaction parties, is often criticized. Spending hours on hold while waiting to speak with a customer service representative is not the best way to spend your day.

Stripe is one company directly benefiting from PayPal’s lack of customer service. They’re taking market share in part by offering 24/7 customer support.

3. Delays to transfer out of PayPal

Money moves fast in our hyper-digitised age and corresponding thirst for rapidity. It may (or may not) surprise you to learn that PayPal will hold your funds for 3-5 business days before they clear into your PayPal account. Emphasis on ‘business days’ with weekends adding two more days on top.

Technology is more than capable of transferring funds instantly. Many of its competitors demonstrate this capability by offering 1–2-day transfers, or even instant payments.

PayPal chooses to hold funds in their accounts to gain interest on them for a few days. They claim that this delay is due to the use of a clearing house – an institution that checks and approves the transfer of funds before their deposit. However, this claim is weakened by the fact that PayPal will happily waive the waiting period for a fee.

4. PayPal holds your crypto

In 2021, PayPal introduced a revolutionising new feature to the platform: cryptocurrency. PayPal introduced four cryptocurrencies: Bitcoin, Ethereum, Litecoin and Bitcoin Cash, which can be used like regular currencies to make purchases on the platform. Enabling 392 million users to access to cryptocurrency was viewed as a huge boost for the crypto industry.

However, there is one large problem with their cryptocurrency feature – users can buy, sell, and make purchases with cryptocurrency, but they cannot transfer. This effectively locks your crypto to your PayPal account.

There is a common phrase in the crypto world: ‘not your keys, not your crypto.’ For more experienced crypto users, the inability to transfer your crypto is a significant hindrance.

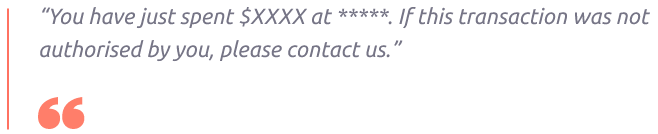

5. Most credit cards have a fraud protection guarantee

If you have a credit card with Visa, Master Card or American Express, then you may have received a text, in-app or email notification when making larger purchases. They typically read something to the effect of:

This is your card provider checking irregular payments made to your card and offering help in the instance that is a case of fraud. This level of service is unparalleled in the digital payment space and reiterates the safety of using traditional finance networks.

By contrast, PayPal adopts a much less proactive stance against fraud. While protection is provided to an extent, the onus largely falls on the consumer to monitor for fraudulent transactions, especially in the realm of e-commerce, and take action when necessary.

As roughly a third of fraudulent transactions and scams go unreported, many consumers seem unaware that they are victims of fraud at all. PayPal’s reactionary approach can leave many consumers vulnerable to financial crime and without the proper means to defend against it.

To wrap up

With PayPal’s disproportionate fees, relatively poor customer service, murky holding times, confusing cryptocurrency restrictions, and improper fraud prevention, it’s unsurprising that there’s a growing shift among users toward exploring alternative platforms. While Paypal market dominance remains strong, as consumers become more financially literate and aware of their checkout and payment options, a shift towards other financial services is likely.

References

1. “When-and why-did people first start using money? Source: https://theconversation.com/when-and-why-did-people-first-start-using-money-78887

2. “PayPal raising merchant fees on some of its transactions” Source: https://www.theverge.com/2021/6/19/22541286/paypal-raise-seller-fees-transactions-online-payments

3. Scams Cost Australians Over $630 Million” Source: https://www.scamwatch.gov.au/news-alerts/scams-cost-australians-over-630-million

Subscribe to Our Blog

Stay up to date with the latest marketing, sales, service tips and news.

Sign Up

"*" indicates required fields